Winter

2016

grainswest.com

11

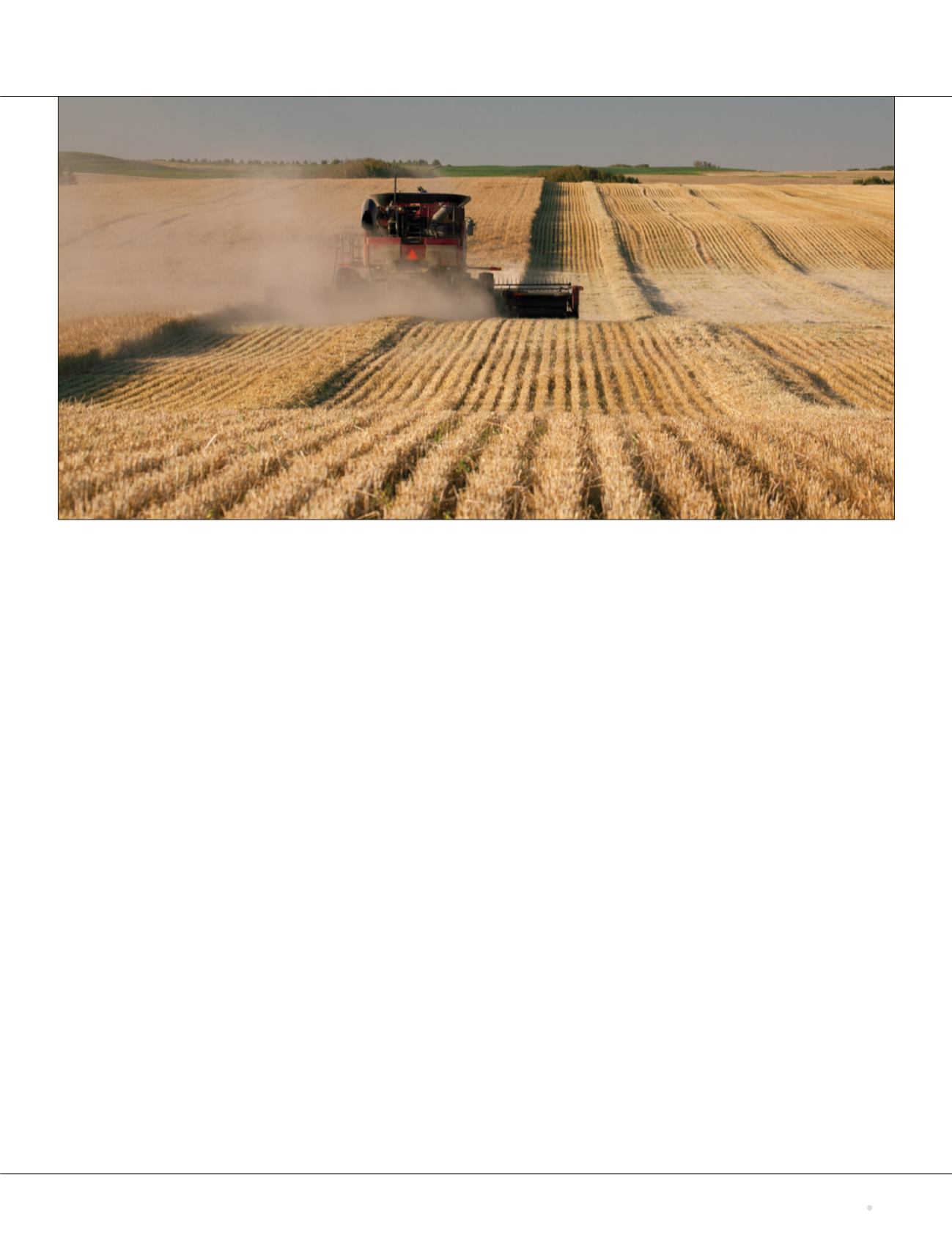

Rain showed up just in time for some producers, salvaging what had been a very dry crop, while others received toomuch rain during harvest, downgrading quality.

Photo: Michael Interisano

The rest of May through August was dry.

“We got maybe one- or two-tenths of rain

here and there but it didn’t do a lot,” he

said. “The end of June and early July is a

critical time for moisture for cereals and

we were very dry. There were some later

showers that helped the canola, but any

moisture we got after mid-July didn’t help

the wheat.”

Some showers did show up in early

September to interrupt harvest. With

the risk of rain, and wheat that had very

weak straw, Heck decided to combine

and dry the wheat before the standing

crop went down.

“Overall, we were disappointed with

the wheat crop,” he said. “Wheat was

below average but the canola was surpris-

ing, as it came in at about average. We

were dry here but it was quite variable.

Some areas in the Peace had one inch of

rain, and then you went three miles away

and they had 4.5 inches. We were luckier

than some.”

PRICES HOLDING

Yields just below or near average reflect

the mood of commodity markets heading

into winter, said Neil Blue, an Alberta

Agriculture and Forestry market analyst

based in Vermillion. There doesn’t appear

to be any dramatic news one way or the

other Blue said, as he looked at late-fall

supplies and price outlooks.

“Wheat right now, for example, is pretty

flat in terms of price,” Blue said. “Wheat is

obviously a commodity on the world mar-

ket and the world was pretty well supplied

with wheat this fall. We are seeing a lot of

different grades out there, which will fit

in a range of markets, and really that is a

good thing.”

While in the coming months there

could be some weather-related rumours or

developing issues affecting wheat pro-

duction, which could affect prices, Blue

said, “Overall, at the moment I don’t see

anything that is really going to push the

market in any particular direction. Prices

are pretty flat right now, and I would say

it is a good time for producers to watch

for basis opportunities as well as forward

pricing opportunities to capture some

carrying charge in the market.”

Looking at feed grains, such as barley,

he said there were no strong signals for

price change in late fall. Calf prices had

dropped, and feeder margins were tight

or negative, and that could weigh on

feed grain prices. However, feeder cattle

exports to the U.S. (as of late November)

are 25 per cent lower than last year,

implying more cattle to be fed here in

Alberta this winter. Also, with limited

supplies of hay this year, producers could

be using more grain to feed with straw

as an alternative wintering ration. Blue

expects feed grain prices to slowly

improve during the winter, but the

degree of that improvement will depend

on winter weather.

Similarly, he didn’t see anything major

on the horizon with canola prices heading

into 2016. Canadian and world production

of canola was down in 2015. However,

there is increased crush capacity in Can-

ada and overall supplies are fairly tight. “I

don’t see anything crazy happening with

canola prices, but again it is a good time

for producers to watch for basis opportu-

nities when marketing.”

Blue said field pea prices, particularly

yellow peas, have been a shining star, with

late-2015 prices as high as $10.50/bu,

and forward contract prices for next

September of $9/bu. The main driver has

been demand from India, which is still

overly dry in some production areas after

two seasons of below-average yields. Len-

til prices are also very good, with current

prices of 40 to 50 cents per pound and

new crop bids of 30 to 36 cents per pound

for most types.